European banks and financial institutions expect credit impairments to increase

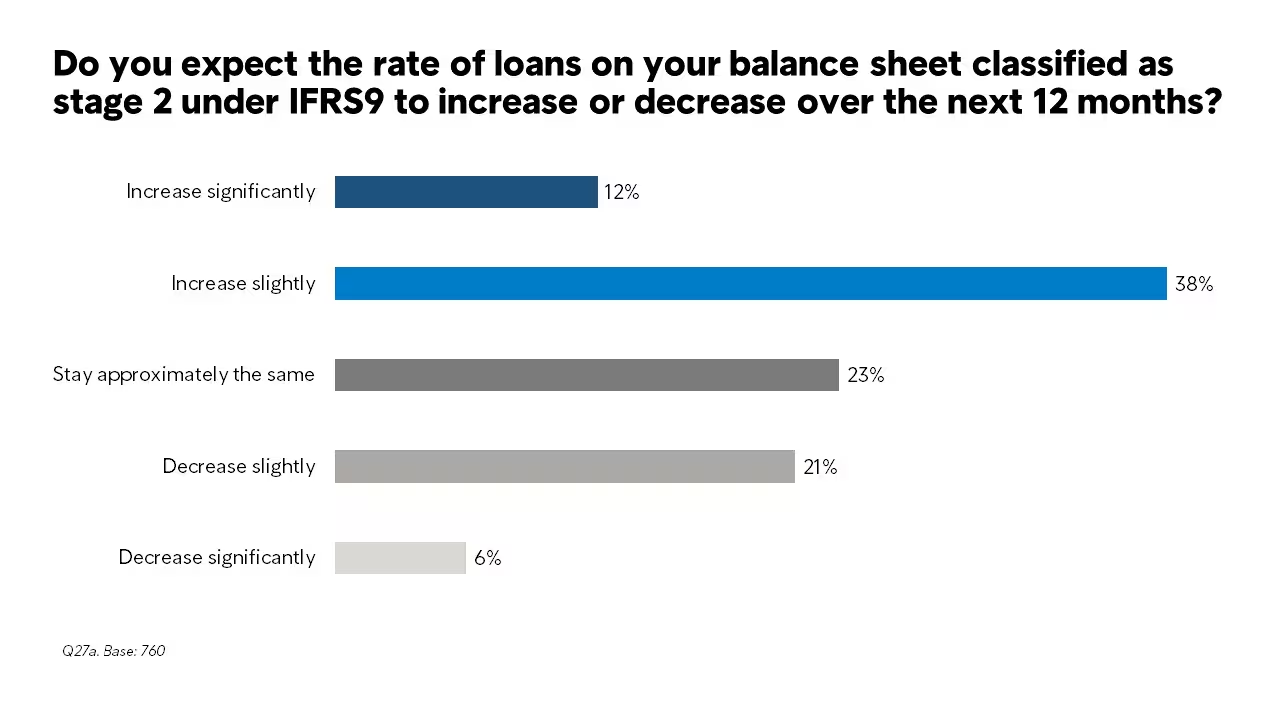

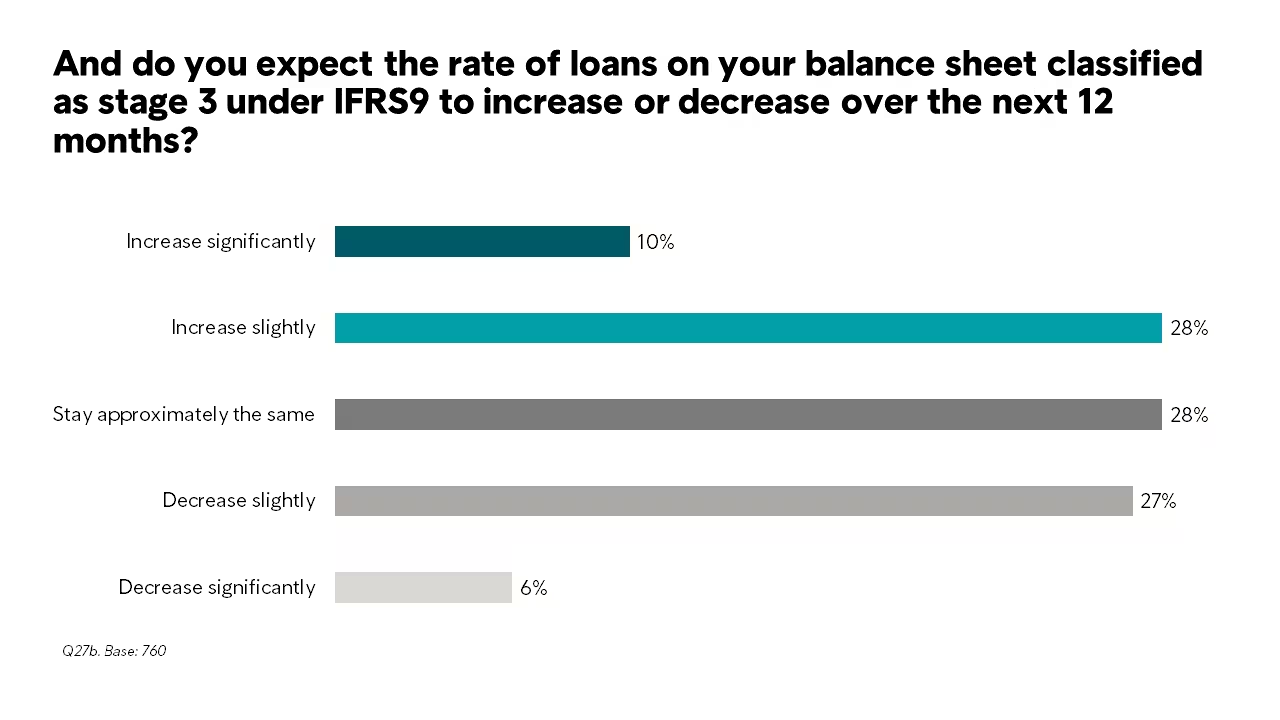

The macroeconomic environment has started to impact the quality of credits on European banks and financial institutions’ balance sheets. Intrum’s yearly European Payment Report (EPR) shows that half of the surveyed financial institutions expect the rate of their loans classified as stage 2 under IFRS9 to increase during the remainder of 2022, and close to 4 in ten (38%) also believe that their share of stage 3 loans will grow.

In the wake of surging inflation and rising interest rates, Intrum’s annual European Payment Report, a survey of 11,000 European companies of which 760 were banks and financial institutions, points to increased risk for late and non-payments during the remainder of this year.

Half (50 per cent) of the respondents from European banks and financial institutions believe that the rate of loans on their balance sheets classified as stage 2 under IFRS9 are to increase during 2022, and 38 per cent also expect the share of credits classified as stage 3 to grow.

Europe is in the midst of a very turbulent macroeconomic environment and an increasing number of indicators suggest that we could be facing a period with stagflation; a combination of high inflation and contracting economic output.Anna Zabrodzka-Averianov, Senior Economist at Intrum

“This will elevate the risk for credit impairments across the economy, including for bank loans. While the NPL ratios have continued to decrease so far this year, stage 2 loans are on the rise, as shown by the latest EBA Risk Dashboard for 2022Q2. There are a number of uncertainty factors surrounding the future economic outlook in Europe, but it is likely that we will see continued growth of loans classified as stage 2 but also eventually stage 3 during the coming months”, says Anna Zabrodzka-Averianov, Senior Economist.

Intrum’s European Payment Report also shows that 8 in ten (80 per cent) of the participating financial institution respondents ranked improved management of credit risks on top of their strategic agenda for the year.

About the IFRS 9 definitions of credit impairment

Stage 1

Credits are classified as performing, meaning that they have not deteriorated significantly since recognition and it is likely that the individual or company liable for the loan is will be able to pay interest and amortizations as agreed.

Stage 2

Credits are associated with an increased credit risk. These credits are not yet associated with an objective evidence of a credit loss, but it is relatively likely that the individual or company liable for the loan will not be able to make all payments as agreed.

Stage 3

Credits are classified as non-performing, meaning that there are objective evidence that the credit has impaired, as the individual or company liable for the loan has or is about to cancel one or several payments.

Source: Financial Instruments: Expected Credit Losses

About Intrum’s European Payment Report 2022

The European Payment Report describes the impact of late payments on businesses’ outlook, growth, and development. The report is based on a survey conducted simultaneously by Longitude in 29 European countries between 17 January and 13 April 2022. In total, 11,007 small, medium and large companies across 15 industry sectors participated in the research. The target group for the survey include subject matter experts within finance departments in addition to C-level executives.