Young, free and… in debt?

Younger consumers are displaying behaviours that suggest they are less financially savvy than their parents. Having grown up in a low interest rate and low inflation environment, they may be unprepared for the challenges of operating in more challenging economic conditions.

Increasingly using buy-now, pay-later solutions, not keeping track of their spending and are likely to have lower incomes than older consumers. How can they stay on top?

Buy-now, pay-never?

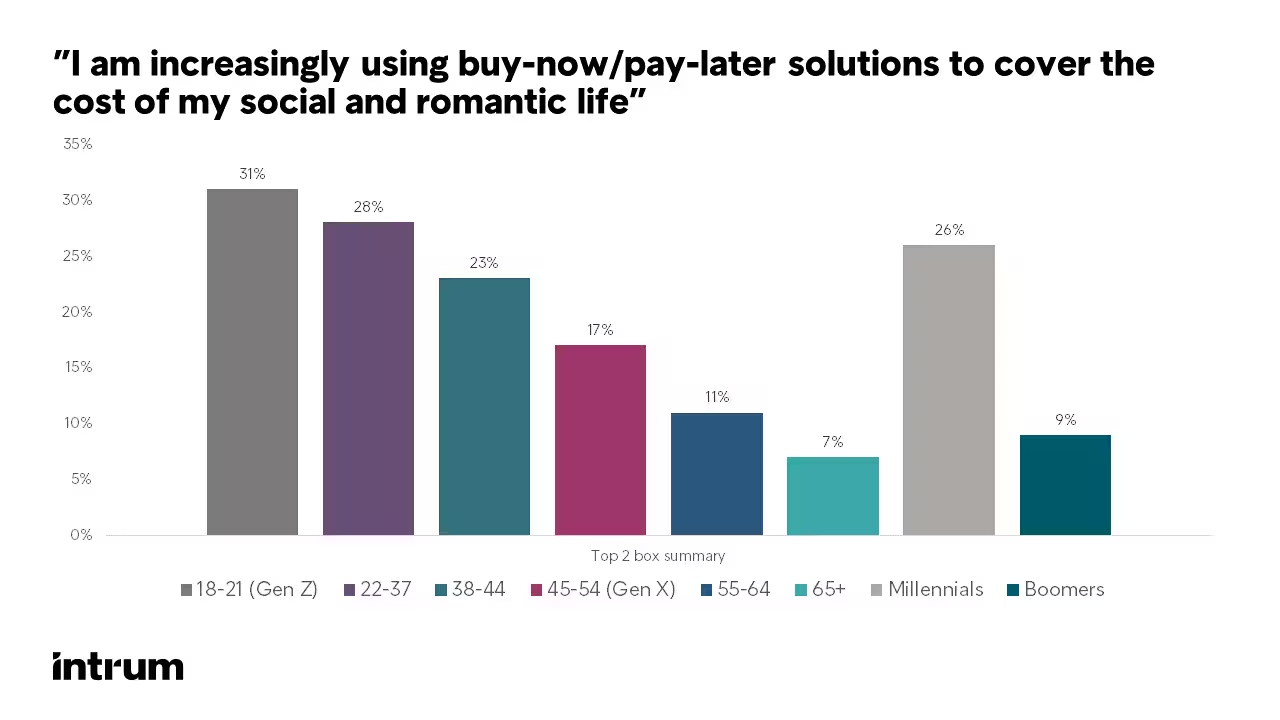

According to our research, younger consumers are much more likely than their parents to use buy-now pay-later solutions to cover the cost of their social and romantic life. Almost a third (31 per cent) of the Gen Z cohort in their late teens and twenties say are doing so, compared with 9 per cent of the boomer generation.

This may seem like an obvious solution to the problem, but stacking up debts can lead to big problems and it’s crucial younger consumers understand what they’re signing up to.

While credit plays an important role in keeping society running and enabling us to achieve our dreams, it’s essential to stay on top of repayments and ensure you can meet your monthly commitments – if not, they risk extra charges, fees and debt collection actions.

Buy-now, pay-later can turn into a debt problem if not managed carefully. Younger consumers should think hard before paying for their social life this way. Is a night out now worth the hard slog later?

Take the time to stay on top

Younger consumers are more likely to say they have lost track of their monthly spending than their older peers. For example, a fifth of millennials say they have lost track of how much they spend each month on digital subscriptions, compared with six per cent of boomers.

As younger consumers are likely to be on lower incomes, it’s easy for them to get disheartened and stick their heads in the sand when it comes to money. In fact, a quarter of 18-21 year olds say they don’t even want to know how much they owe in total.

While this is understandable, the key to avoiding debt problems is to stay on top of your budget, know how much money you have coming in and going out each month, and tailor your lifestyle accordingly.

Save for the future

There is good news on savings. Although younger consumers are likely to have less disposable income early in their careers, 88 per cent of Gen Z and 82 per cent of millennials are putting away some money each month, compared with 72 per cent of Gen X 45-54 year olds.

A good savings habit is the basis of strong finances, enabling consumers to cope with unexpected expenses. A quarter of those in their late teens and early twenties who save said this is the reason they are putting money away. Another 18 per cent are saving for travel, while 12 per cent said they are putting money aside to buy a house or apartment.

Starting good financial habits at a young age means consumers can achieve their ambitions free from the worry of problem debt. However, if you run into difficulty there is help. At Intrum we specialise in working with people to resolve their financial problems and get them back on track. It is never too late.