How to choose the right invoice management software

Late payments are no longer a cash flow inconvenience. They are a structural barrier to growth.

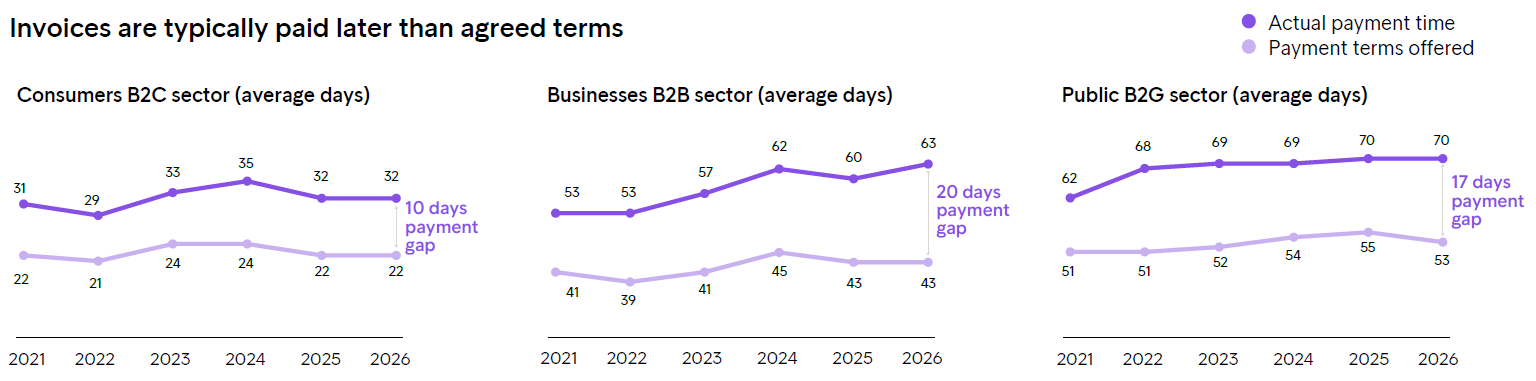

Almost six in ten European business executives say they are more concerned than ever about their customers’ ability to pay on time, according to Intrum’s European Payment Report 2026. The average of B2B payment terms has increased from 60 to 63 days the past year, with an average 20 days payment gap delay (time between payment terms offered and actual payment time). In B2C payments companies report an average payment delay of 10 days from the payment terms offered to actual payment

Businesses are being paid later than before

That is where digital invoicing and a connected invoice-to-cash process make the difference, not as an IT purchase, but as a business-critical decision. This guide covers what invoice management software does, the capabilities that matter most for B2B businesses, and the questions worth asking before committing to a platform.

What invoice management software actually does

Invoice management software handles the creation, delivery, tracking, and reconciliation of invoices. In a well-configured system, that covers the full cycle from raising a bill after a sale to recording the payment against the right account.

The difference between a strong and a weak platform typically shows up in two areas: visibility and integration. Visibility means knowing, in real time, which invoices have been sent, which have been opened, which are approaching their due date, and which are already overdue. Integration means those records are connected to a payment processing platform and the business's own accounting system, allowing settled invoices to reconcile automatically rather than requiring manual matching at the end of the month.

Without both perspectives, the invoicing process creates work rather than reducing it. Finance teams find themselves chasing information across systems, manually cross-referencing payment records, and reacting to overdue invoices after the fact rather than anticipating them.

The capabilities that matter most

Billing requirements depend on who you are invoicing. Businesses invoicing other companies (B2B) typically deal with higher invoice values, longer payment terms, and structured approval processes on the customer side. Businesses invoicing consumers (B2C) face a different set of demands: higher volumes, shorter payment windows, and the need for a frictionless payment experience. Whatever the customer segment, a platform chosen for simplicity alone will fall short.

Invoice creation and delivery

The platform should generate invoices directly from business data, purchase orders, contracts, or service records, and deliver them through the channels the customer uses. For business customers, that often means a standardised e-invoice format. For consumers, digitally delivered dynamic invoices are increasingly common and consistently produce faster payment responses.

The EU's move toward mandatory e-invoicing means that digital invoicing compatibility is becoming a compliance requirement across a growing number of European markets. Germany mandated the ability to receive structured e-invoices from January 2025. Belgium follows from January 2026. France begins its phased rollout for large companies from September 2026. The ViDA (VAT in the Digital Age) package, approved by the EU Council in March 2025, sets the framework for mandatory intra-EU e-invoicing from 2030.

Businesses evaluating platforms now should confirm they are building on a foundation that meets both current and forthcoming regulatory standards across their operating markets.

Recurring payments and automated billing

For businesses with subscription models, retainer-based services, or any repeating billing arrangement, recurring payments are not an optional feature. The platform should allow payment terms, billing frequencies, and customer authorisations to be configured once and executed consistently, without manual intervention each cycle.

Automated, predictable billing also removes a specific and common driver of late payment: the invoice that was never clearly received, or the approval workflow that was never triggered. When billing runs reliably, customers on the receiving end can settle on time without having to chase for documentation.

Real-time visibility and reporting

Finance teams need to see receivables as they actually stand, not as they stood at the last month-end close. Strong invoice management software provides a live view of the billing ledger: what has been issued, what has been received, what is approaching its due date, and what is already overdue.

When invoices are approaching their due date with no payment received, finance teams can act before the deadline rather than chase after it. Across hundreds of accounts, that picture needs to be clear and accessible, not buried in exports and spreadsheets.

Payment integration and methods

An invoicing platform should be directly connected to a payment processing platform. When a customer receives a digital invoice, they should be able to settle it through their preferred method. For consumers, that means card, digital wallet, or open banking directly from the invoice. For business customers, it means smooth integration with their accounting or ERP system, supporting bank transfer, direct debit, or open banking without manual intervention.

Payment integration removes friction at exactly the point where many invoices go unresolved for longer than they should. Whether the customer is a business or a consumer, the path from invoice to payment should be as straightforward as possible.

Payment automation and reminders

Manual follow-up is inconsistent and slow. It depends on a member of the finance team noticing that an invoice is overdue and finding time to act. Payment automation handles that systematically, sending reminders at configurable intervals relative to the due date and escalating through defined stages when payment does not arrive.

The scale of the opportunity is significant. According to Intrum’s European Payment Report 2026, businesses across Europe currently spend around €386 billion a year on staff time dedicated to chasing late payments. The report estimates that AI tools in payments management already save businesses around €106 billion annually in labour costs, offsetting about one fifth of the costs they would otherwise face. This highlights the potential of AI-enabled payments management to improve efficiency, reduce late payments and strengthen customer engagement.

→ Intrum’s European Payment Report 2026

Collections escalation

Not all late invoices resolve through reminders. When a customer does not pay after repeated follow-up, the business needs a documented path to escalation. The strongest platforms handle the handover from billing and reminders into a collections workflow without requiring manual intervention to bridge two separate systems.

That continuity matters operationally and relationally. An escalation process that carries the full billing history, what was sent, when, and what response was received, supports a more considered and constructive approach than one that begins from scratch with incomplete information.

Late payments harming your cash flow?

We help you free up cash tied in unpaid invoicesWhere invoice management breaks down

Understanding the most common failure points in invoice management helps clarify what to look for in a platform and what to address in the setup process.

- Incomplete invoice data: invoices that lack a clear description, accurate pricing, or the correct customer reference are more likely to be disputed or deprioritised by the customer’s accounts payable team.

- Mismatched payment terms: when the terms on an invoice differ from those in the underlying contract, the customer has a legitimate basis to delay.

- No follow-up process: without a defined reminder and escalation sequence, overdue invoices accumulate without action.

- Poor visibility across accounts: businesses managing large invoice volumes without a centralised view tend to miss early warning signs and respond too late.

- Disconnected systems: billing, payment processing, and accounting held in separate tools with no integration between them forces manual reconciliation and creates data gaps.

Most of these problems are structural rather than attitudinal. They reflect the constraints of the tools and processes in place, not a lack of effort by finance teams.

Questions to ask when evaluating platforms

The questions below are a practical starting point for any evaluation. They are designed to surface the capabilities that matter most for B2B invoice management, rather than the features most prominently positioned on product pages.

- Does the platform cover the full invoice-to-cash cycle, from invoice creation through to payment reconciliation, or does it require additional tools to complete the process?

- Can it deliver invoices in the formats your customers require, including standardised digital invoicing formats for markets with mandatory e-invoicing requirements?

- Does it support recurring payments and automated billing for subscription or contract-based revenue?

- What payment methods does it accept, and can customers settle invoices directly without navigating to a separate system?

- How does the platform manage the transition from overdue reminders to collections activity?

- What does the reporting suite show, and can finance teams access real-time receivables data without manual extraction?

- How does the platform integrate with existing accounting and ERP systems, and what does a realistic implementation timeline look like?

That last question deserves particular attention. A billing platform that takes six months to configure and requires ongoing IT resources to maintain may deliver less practical value than a more straightforward option that finance teams can operate independently. Complexity is not the same as capability.

The difference a connected platform makes

The strongest case for integrated invoice management software is not any individual feature. It is the compounding effect of a connected process. When billing, payment, and collections run through the same platform, each stage benefits from the information generated by the others.

Finance teams work from a single view of each customer’s position. Automated actions trigger at the right time, based on actual customer behaviour rather than scheduled calendar reminders. Escalation, when it is necessary, begins with the complete picture. Reconciliation becomes a system function rather than a manual task.

For businesses processing high invoice volumes, or managing complex B2B relationships across multiple markets, that coherence has a measurable effect on days sales outstanding (DSO), staff time, and the quality of customer relationships. Businesses that have adopted AI-powered payment tools report efficiency gains, fewer late payments, and stronger customer engagement as the three leading outcomes, according to Intrum’s European Payment Report 2026.

→ Intrum’s European Payment Report 2026

Where to start

Selecting invoice management software does not need to be a long or complex project. The most effective approach is to begin with a clear picture of where the current process breaks down, whether that is poor visibility, slow invoice delivery, manual reconciliation, or inconsistent follow-up, and choose a platform that addresses those specific problems first.

A single three-month pilot, run across a defined set of accounts, is usually enough to know whether a platform is working and what needs adjusting before a wider rollout. Three metrics are worth tracking from the start: average days to payment, the proportion of invoices settled by their due date, and the staff time spent on manual invoice-related tasks.

Improving those numbers is not a technology problem in isolation. It requires a clear process, accurate data, and consistent execution. The right platform makes all three significantly easier to achieve.

Improve your invoice and payment process

Effective invoice management helps businesses get paid faster, improve cash flow, and create a simpler payment experience for customers.